Butler National Corporation (BUKS) Q3 Earnings

EARNINGS: Strong quarter driven by Aerospace & sportsbook growth and reduced debt

See my original investment case on BUKS here: Butler National Corporation (BUKS)

Butler National Corporation’s Q3 earnings were released on March 16th. Future blog posts on quarterly earnings should be shorter since not a lot happens each quarter, however I wanted to include a few additional ideas to supplement my original investment case, which can be found here: Original investment case.

I identified the following KPIs, or metrics, I was looking for going into Q3 earnings and below is an excerpt from my last BUKS blog post:

These metrics were created to help objectively assess (1) what I would consider a good quarter and (2) help support that management is making good decisions. Beating quantitative metrics can be a good sign that the company is moving in the right direction, but there are qualitative factors to consider as well.

Many things can influence an individual quarter’s results so if BUKS hits on all of the metrics, two of the metrics, or none of them it may not tell us much - this quarter’s results won’t matter five, three, or even two years down the road. Try to keep a long-term mindset.

So how did BUKS do? Spoiler alert: they hit on all metrics.

YoY Revenue Growth in both segments:

We saw quarterly growth in both business lines year-over-year (YoY):

It is good to see both lines of the business are growing.

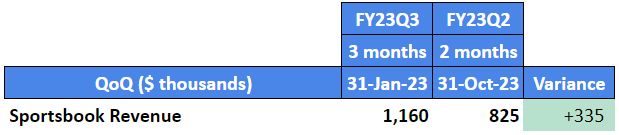

>$1.0M sportsbook revenue in the quarter:

I wanted to see that the $825K ($413K per month) in the first two months of sportsbook operation was repeatable. Note: the online sportsbook opened for bets September 1st, so there were only two months of operations included in the last quarter ended October 31st.

This quarter (Q3) includes three months of operations and we saw $1.2M ($387K per month) in sportsbook revenue:

The annual run rate of the Sportsbook is now $4.8M per year ([$1,160K + $825K] / 5 months * 12 months). We can use the annual run-rate as a rough guide because (1) it is too early to get a reliable estimate what the sportsbook will earn going forward and (2) depending on your assumptions revenue per month could go up or down from here. I’ve included some qualitative factors that could have influenced historical and may influence future results below:

Was there an early influx of players due to the recent legalization of online sports betting in Kansas i.e. pent up demand? This could suggest revenue per month is overstated.

Most businesses start with a base of customers and grow from there i.e. you pay to acquire a customer, through marketing or otherwise, but their lifetime value is often spread over months or years. This could suggest revenue per month is understated.

We see DraftKings is growing their revenues and in their most recent quarterly earnings revenue grew 81% YoY. This could suggest revenue per month is understated. However we don’t know how much growth is related to acquisitions & new markets versus organic growth i.e. land-based sports bettors moving online or players enjoying online betting’s efficiency, thus spending more.

BUKS hasn’t launched Bally’s online offering yet. This could suggest revenue per month is understated.

I think $4.8M is a reasonable estimate for the first year of sportsbook operations, but for what it’s worth, I would guess sportsbook revenue grows beyond $5M per year in the future due to points #2, #3, and #4 above.

Operating Leverage

I know what you’re thinking… $5M on a company that makes $74M in revenue a year, so what? That’s only 7% growth!

My argument is that not all revenue is the same - revenue that earns higher gross margins, or is growing faster, is worth more and should command a higher multiple.

As I mentioned in my previous post, DraftKings provides a turnkey solution and the only cost to Butler National is (1) the cost of the physical in-person sportsbook which required upfront capex & likely requires additional staffing, and (2) the commission they remit to Kansas State (if it isn’t already being netted out).

My theory is that the revenue earned online through the sportsbook is high margin incremental revenue and most of this revenue will fall to the bottom line i.e. the online sportsbook doesn’t add material fixed or variable costs to BUKS.

Here is an example:

Let’s say going forward BUKS makes $4.8M a year on the sportsbook, they have 20% costs (turn-key solution), and a 27% tax rate. We end up with $2.8M net earnings ($4.8M * [1 - 0.80] * [1 - 0.27]).

BUKS made ~$10M in earnings last year (FY22), with a market cap of $50M which put them at a Price to Earnings of 5 (cheap). It appears they will make less this year as they have only made $5M so far in three quarters (not adjusting for the one-time severance cost discussed in the operating profit section below).

This implies a +28%, or greater, ($2.8M / $10M) increase in earnings and doesn’t factor in any growth of the sportsbook from current levels.

So even though we projected the sportsbook would increase BUKS overall revenue by 7% in the first year, earnings could grow by a lot more. Over the long-term stock prices tend to follow the change in a company’s earnings.

We haven’t seen this operating leverage in the results yet as overall operating margin for the Professional Services segment dropped from 25% to 24% YoY. This could be influenced by other factors (marketing, additional staffing costs related to the temporary in-person sportsbook, etc.) or I could be wrong.

The Professional Services operating margin % will be something to monitor going forward.

A couple quick thoughts on upcoming quarters:

Do you think a lot of people in Kansas placed bets on the Super Bowl in February when the Kansas City Chiefs defeated the Eagles? It could be a nice boost to sportsbook revenues in the upcoming quarter, or the reverse if many people won betting on the Chiefs.

If in the next quarter (FY23Q4) we see a spike in sportsbook revenue, then in the following quarter (FY24Q1), without the benefit of the Super Bowl, we could see a subsequent drop in revenue.

Sports betting is cyclical and big events (Super Bowl, World Series, World Cup Soccer) drive betting at different times of the year.

>$2.5M overall operating profit

$2.5M operating profit is a conservative profit estimate based on previous quarters. Operating profit can fluctuate quarter to quarter, but of course it is a good sign when the company’s operations are consistently profitable.

Although we met our profitability metric, overall operating profit was down 15% quarter-over-quarter (QoQ) and 23% year-over-year (YoY). However, when we dive into the notes to the financial statements we see a $1.3M severance accrual which was not included in the news release:

Diving further, a press release on January 26, 2023 states: “Effective January 20, 2023, Craig D. Stewart's employment with the Company was terminated. Mr. Stewart remains on the Company's board of directors.”

As a reminder Craig is a related party, Clark Stewart’s (CEO) son, and the entire $1.3M appears to have been charged in Q3 to the Aerospace segment.

I don’t have any insight into the cause for termination, but it could have been on good terms as he still remains on the Board. It is interesting that they didn’t include a mention of the severance in the earnings press release.

Per simplywall.st Craig was making ~$500K per year (5% of FY22 net income):

He is still on the Board and other independent directors are making $24K to $48K per year. So, while I’m not sure if he needs to be replaced, this could save approximately $400K+ per year for the company.

After we adjust our operating profit above to remove the $1.3M charge in Q3, here are the updated numbers (27% tax applied):

Operating profit increased 17% QoQ and 6% YoY, with almost all of the growth coming from the Aerospace segment.

Net debt goes down

The company’s positive book value makes up almost the entire $50M market cap and they don’t hold excessive levels of debt. As most of their debt is carried at between 5% to 6% interest rates, one could argue there are higher ROI uses of cash elsewhere, but I think paying down debt is an easy (hard to do wrong) use of capital and it limits our downside risk.

Total debt is down $1.3M and net debt is down $4.0M vs the prior quarter, this looks good to me.

Capital allocation

Their cash balance is significant & growing ($17M as of FY23Q3) and while they have been buying back their own shares, they could do more buy-backs - especially if we think the stock is currently underpriced.

A few potential initiatives depending on the ROI:

New FAA approvals & Aerospace products

Additional hangars ($27M Aerospace backlog as of Q3). Although let’s wait to see the ROI on the recently built hangar.

In-person sportsbook marketing locations. Again let’s wait to see how the Boot Hill sportsbook does. I think the online offering is much higher margin & ROI anyways.

Management will have a better idea on the best use of capital, but I think buy-backs or implementing a dividend, now that the company has proved consistent profitability, would certainly benefit shareholders.

Conclusion

Overall, it looks like a good quarter to me. So what am I going to do now?

As I believe Butler National Corp’s management team has improved the business and its long-term outlook, I will buy more shares. The Art of Execution by Lee Freeman-Shor is a good book to read on the principle of adding to companies with improving fundamentals (not necessarily price) and avoiding doubling down on companies with deteriorating fundamentals.

See my next article on BUKS here: Butler National Corporation (BUKS) May 12 PR

Disclaimer: As of March 19, 2023, I am a shareholder of Butler National Corporation at an average cost base of $0.67. My plan at the time of writing is to hold these shares long-term, but I may have sold my position by the time you’re reading this. This is not a purchase recommendation and I can only hope that I’m right on 3 out of 5 (60%) investments I make — this could be one I’m wrong on. Please do your own research and double-check my data & findings.