Kits Eyecare Ltd

Large TAM; Strong management; Growing eyeglass segment

Current price (KITS.TO): $4.01 CAD

Current market cap (KITS.TO): $125.6M CAD

Kits Eyecare Ltd. has strong, aligned management and is currently transitioning from an unprofitable company with flat revenue to a self-funding, double-digit growth story. Gross margins, revenue growth, and cost structure have consistently improved since the January 2021 IPO. Kits feels like an asymmetric bet - heads I win, tails I don’t lose much.

Kits is a vertically integrated digital eyecare company that began selling contact lenses and has since entered the eyeglass market in Canada and USA. Kits came public in January 2021 at an initial offering price of $8.50 and the price precipitously dropped to the mid-$2 range and stayed there until recently, when it appreciated to its current price of $4.01.

Management, Integrity, and Alignment:

The Company is run by its three founders: Roger Hardy (CEO), Sabrina Liak (President - previously with Goldman Sachs), Joseph Thompson (COO - previously with Amazon), as well as Arshil Abdulla (CTO) who ran LD vision group, Kits predecessor, for over 10 years.

Who is Roger Hardy? In 2000, Roger Hardy started Coastal Contacts Inc in a basement office and grew the company to the world’s largest online retailer for eyewear. He started selling contact lenses (low margin) and later expanded into eyeglasses (higher margin) before selling to Essilor in 2014 for C$430 million. This may sound familiar because it is the same path Kits is taking, starting with a base contact lens business and moving into the higher margin eyeglass business.

After selling Coastal Contacts in 2014, Roger used part of the proceeds to acquire several shoe companies and entered the competitive business retailing shoes online. This company eventually filed for bankruptcy, but would have provided valuable experience and multiple learnings in the online retailing space.

Since then, Roger has been involved in various projects through Hardy Capital and recently co-founded KITS in 2019. Instead of starting from zero, Hardy Capital purchased LD vision group - a seller of contact lenses since 2002 with approximately $50M in revenues. LD Vision Group was successfully ran by Arshil Abdulla, the current CTO, who owns 15% of the outstanding shares of Kits, and his related parties own a further 19%.

Strong management and governance can be especially important in small cap companies to limit downside risk. Roger has 20 years of experience in online retailing and the varied experience of Sabrina, Joseph, and Arshil rounds out the executive team. If you watch the management interviews linked in the appendix you may agree these are high quality leaders. Kits provides an exciting opportunity to invest in proven founders/leaders at a small market cap.

Alignment:

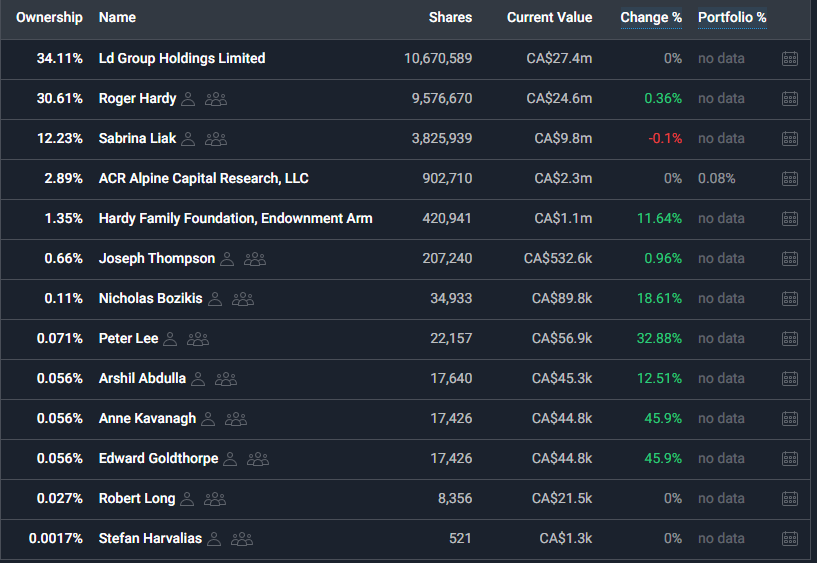

Insiders currently own ~80% of the business, as seen below, so management incentives are aligned with shareholders (source: simplywall.st):

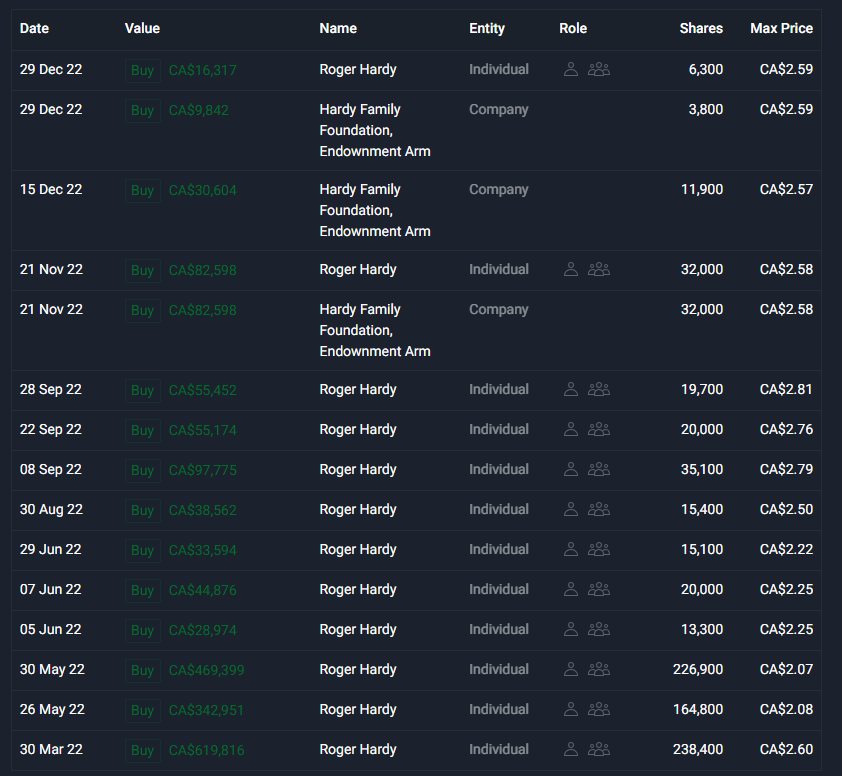

There has also been significant recent buying by Roger Hardy below $3:

Financials:

Solvency / Leverage (as of Q3):

$20M in cash

$14M in loans ($2.3M repaid in the last 9 months)

The Company is free-cash-flow positive and net income positive as of the latest quarter (Q3/2022) and both gross margins (from 26% to 31% YoY) and operating expenses as a % of revenue (from 38% to 30% YoY) are moving in the right direction.

As of Q3, Kits makes 69% of their sales in the US and their expenses are primarily in CAD$ which can result in significant foreign exchange gains reported on their financials.

It appears plausible that the company will be able to self-fund operations without needing to issue shares or take on additional debt.

Revenue Growth:

Overall revenue growth has been relatively flat until last quarter (Q3) when it increased by 18% YoY, and in Q4 revenue rose 29% YoY. Even though overall revenue growth had been flat up until recent quarters, glasses/frames revenue (higher margin) has been growing >50% every YoY quarter (+80.6% YoY in Q3/2022; and +63% YoY for the 9-months ended Q3). So growth is accelerating in eyeglasses and the significant contact lens segment (currently ~86% of sales) is hiding it. As eyeglasses make up a larger portion of revenue, overall revenue growth % could accelerate.

Glasses are now the primary focus of the company and its current marketing. Glasses were a new product added to the original $50M contact lens business (LD Vision Group 2018 revenues pre-acquisition).

Gross margins have increased by 9%, from 21.6% in Q2/2021 to 30.6% in Q3/2022, due to the improved product mix and less discounts post-launch. At the recent Needham conference, Joseph (COO) mentioned that they are targeting 35% - 40% GM.

Operating costs have also come down YoY as the company initially spent on marketing to improve brand awareness post-launch.

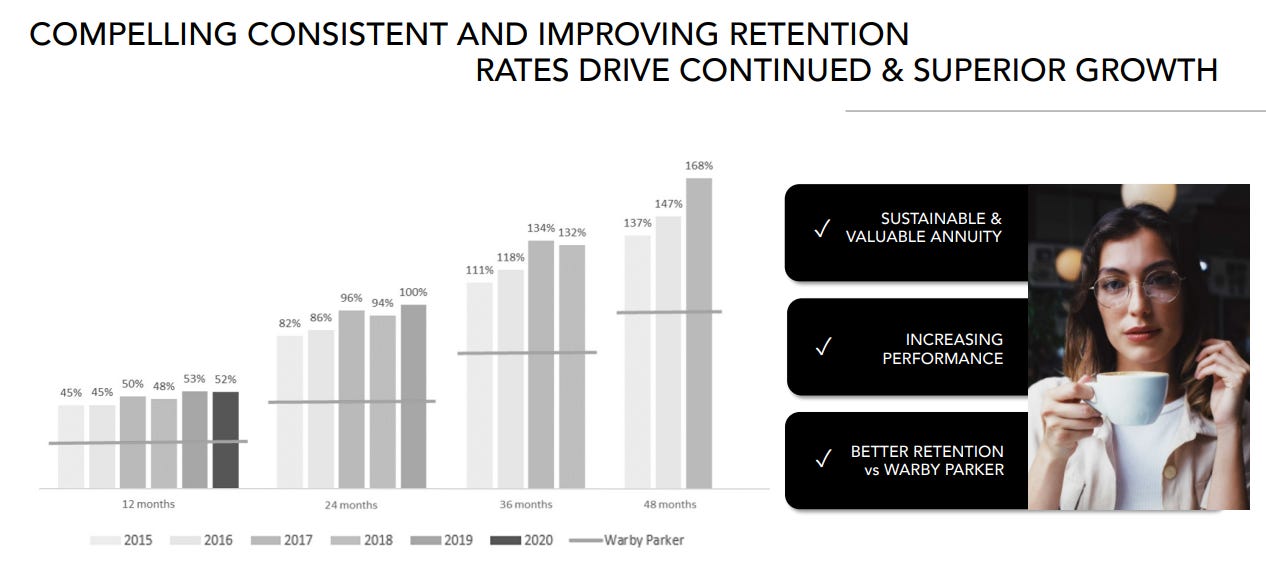

Revenue retention rates (Kits provided below) show that on average customers spend an additional >80% within 2-years; >110% over 3 years; and >130% over 4 years. These percentages are trending up, so year after year customers come back to Kits. This indicates the stickiness of their products and suggests a significant life-time value of a customer. These retention rates are also higher than the category average and competitors such as Warby Parker. With their industry leading customer acquisition cost ($21), and retention rates, it could indicate there is room to increase the marketing spend dial.

Kits has 765K active customers, as of Q3, and added 80K new customers in Q3 (~12% QoQ increase).

Kits recently (Dec 2/22) posted positions for additional warehouse fulfilment staff which supports the fact they are growing and need additional staff to meet demand.

Valuation:

Valuation can be difficult for companies in the growth stage of the business life cycle - it is difficult to put a price on a story of what can be.

The company is currently not meaningfully profitable or FCF positive. However, companies in the growth stage should not be optimizing for earnings and Kits is in the early innings.

Kits is trading at 1.48 Price to Sales (which does not incorporate Q4’s 29% growth) while Warby Parker, a larger competitor ($1.5B market cap), is trading at 2.36 Price to Sales. So Warby Parker is not close to profitability, is only growing ~10% YoY, and is trading at a higher multiple.

For story companies I like to ask myself the question: what does the destination look like 5 to 10 years out; is it plausible (not necessarily probable) that this company could 5x to 10x its market cap in 10 years? I think that is in the realm of possibility for Kits due to their passionate culture, focus on customer satisfaction, and the large eyecare TAM.

Other:

No sign of inventory build-up or obsolescence (YoY inventory decreased)

Moat and Durability of Moat - Competitive Advantage:

Reed Hastings (Netflix) says he has two religions - customer satisfaction and operating profit. Add a strong company culture and you understand Kits’ competitive advantage.

Customer satisfaction:

On-shore manufacturing (quick shipping and returns - customer focus), whereas many online glasses manufacturers have offshored production resulting in declining service levels.

Uses high quality materials for their inhouse brand “Kits” eyeglasses (this inhouse brand makes up most of sales).

Low cost provider (less than 1/3rd cost of in-store glasses) and have the cheapest progressive lenses on the market. As they scale, and costs are spread across a larger revenue base, Kits has the option to pass some of the cost savings to customers, increasing customer satisfaction and putting pressure on less lean competition.

Integration with benefit providers - 2 exclusive agreements so far with Sun Life and Green Shield Canada (customers can purchase glasses through their benefit provider websites and never have to pay out of pocket).

Operating profitability:

Vertically integrated - Newest technology ($10M put into lab after IPO - 70K square feet - highly automated) for production of glasses which decreases labour per pair to single-digits. The facility also has room for additional capacity per their latest call. Note: The manufacturing equipment may be leased, as I don’t see it in the capital asset listing.

Industry leading customer acquisition costs ($21) driven by high net promoter scores, a key KPI tracked by the company (Kits strives to be at or above 80 NPS). Provide exceptional products & service and customers will advertise for you.

Only one physical store (at head office), results in lower overhead costs.

Culture of the company - employees are aligned to the company mission/vision due to strong leadership and above average benefits vs comparable jobs (anecdotal based on latest job postings).

Other Thoughts:

Tailwinds:

Industry - More people using electronics and screens could lead to more near-sightedness and people requiring glasses.

Augmented reality “try-on” software (free to try yourself at their website) will help customers feel more comfortable buying glasses online and digital stores will continue to take market share from brick and mortar. I think online eyeglass shopping is a superior business model to brick and mortar due to lower overhead costs resulting from not needing the physical stores.

Large TAM with little innovation - ready for disruption.

Capital allocation / Acquisitions / Initiatives?

The company is nearing profitability and will be deciding where to allocate excess earnings. I think there are a few options Kits could pursue - invest in new initiatives (technology?), increase marketing spend, pay down debt, pass savings onto customers through lower prices (long-term moat building).

The company focuses on Net Promoter Scores, providing a product and experience so great that the customer will do your marketing for you. If this is the case, is investing in customer satisfaction (technology, savings, and convenience) higher ROI long-term?

A potential future investment could be made in their augmented reality offering - Kits currently licenses its “try-on” software. I think the “try-on” feature is one of the bigger value-add experiences as it allows customers to get an in-store experience digitally, and they can see how the glasses look on their face. I haven’t seen any digital eyeglass retailers that have a seamless, and feature rich, “try-on” user interface yet.

It could improve the customer experience if Kits adds a sorting filter to see “try-on” glasses only, then allows you to quickly switch between, and favourite, different eyeglass frames inside the software. This experience would be more convenient than in-store shopping as I don’t know any stores where you can quickly try on 50 pairs of glasses in 15 minutes and easily keep track of your favourites.

Risks:

Same as any business in the growth stage - Revenue growth plateaus or declines. However, due to customer retention rates and a focus on customer satisfaction the company has been able to grow their glasses revenue while lowering their marketing spend.

Competition - One big player owns most of the market share (EssilorLuxottica). However, their significant size makes it harder to be agile i.e. it would not be shareholder friendly in the short-term to on-shore production, close stores, and compete on margin.

Conclusion:

Anecdotally, I have purchased glasses from Kits and their competitors' sites and I feel Kits offers a valuable proposition - feel (quality materials), price, purchase experience, and fast shipping as they are manufactured on-shore.

This is a story company, if the growth in eyeglass revenue continues and the company keeps costs lean this could be a long-term winner. What to look out for:

Can the company continue to grow their customer base and eyeglass revenue double-digit %? The eyeglass total addressable market is ~4-times the size of the contact lens market.

Can the company stay efficient/lean with their costs? Operating costs as a % of sales should lower with continued growth and scale.

As with any company, does management allocate capital wisely more often than not i.e. high ROI initiatives with a long-term focus? This also depends on the company having such opportunities available.

See my next article on KITS here: Kits Eyecare Ltd: FY23Q1 Earnings and DCF

Disclaimer: As of March 4, 2023, I am a shareholder of Kits Eyecare Ltd at an average cost base of $2.72. My plan at the time of writing is to hold these shares long-term, but I may have sold my position by the time you’re reading this. This is not a purchase recommendation and I can only hope that I’m right on 3 out of 5 (60%) investments I make — this could be one I’m wrong on. Please do your own research and double-check my data & findings.

Appendix - Some interviews you may find interesting:

Roger Hardy interview (Sept 13, 2021):

Roger Hardy & Joseph interview (Dec 1, 2022):

Needham Growth Conference (January 12, 2023):

Quite thoughtfully written and informative, thanks for sharing. This gives sufficient information to assess whether this would be a good LT investment opportunity.